The Supplementary Retirement Scheme (SRS) is a complementary scheme to the CPF and was introduced by the Government on 1st April 2001. The objective of this scheme is to encourage Singaporeans to grow their reserves for retirement.

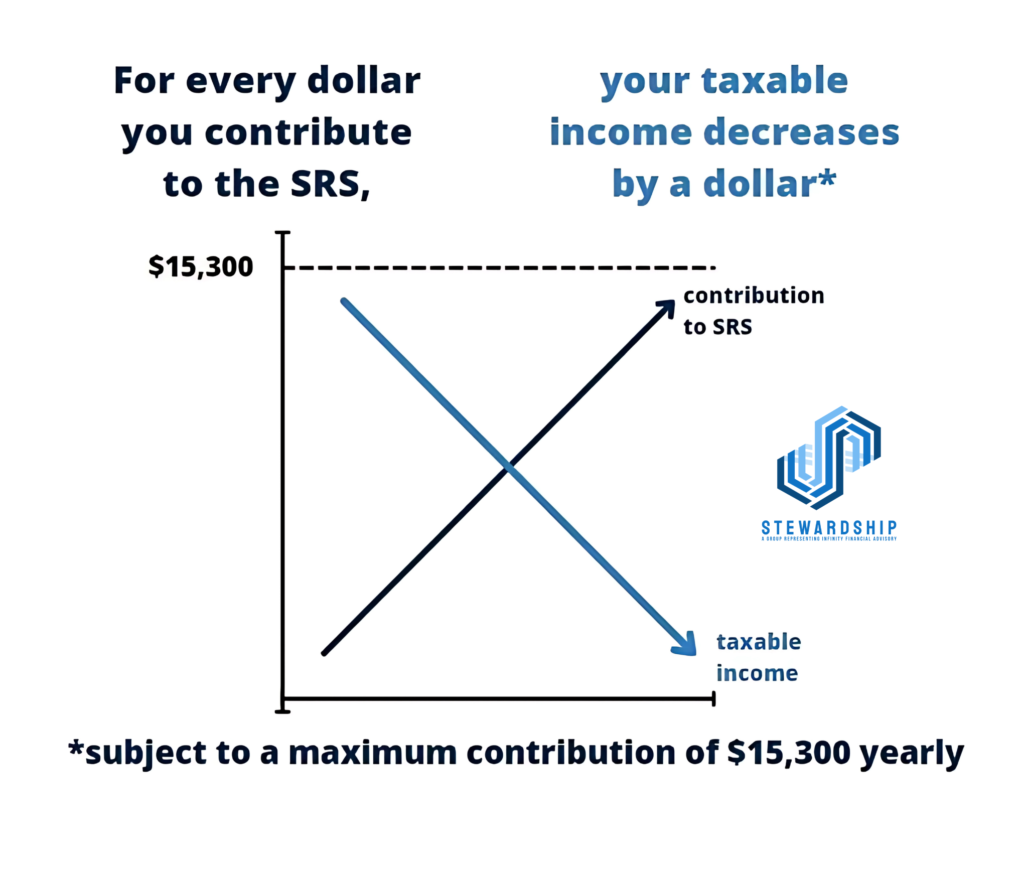

How the SRS works is simple. Your contributions (subjected to a cap) are eligible for tax relief are tax– deductible and your savings will be accumulated in a tax-free SRS account. So generally, for every dollar contribution to the SRS, your chargeable income will reduce by the same amount, subject to a maximum contribution of $15,300 yearly. All you have to do is to open an SRS account with any local bank.

The money you saved in your SRS account may be immediately channelled into suitable investment tools where all your investment gains will also be kept in the same tax-free SRS account until your retirement.

Upon reaching retirement age*, you can begin to withdraw your savings over a period of ten years. 50% of your savings withdrawn each year will be subjected to tax. It is possible to enjoy tax savings if you are able to plan your withdrawals effectively.

The subject of taxation planning contains intricate details that are ever-changing. In such cases, one has to keep up with market trends, new age limits, new monetary limit caps and filing requirements regularly.

With our hectic lifestyles, keeping up to date with all these issues can be quite a handful to juggle with. We then tend to fail to fully understand and analyze how we can practise efficient tax planning. Hence, what you might need is a plan that can help to reduce your chargeable income and enhance your retirement nest egg. Below is an illustration that reflects the amount saved on taxes when one takes up the SRS:

* For illustration purposes only.

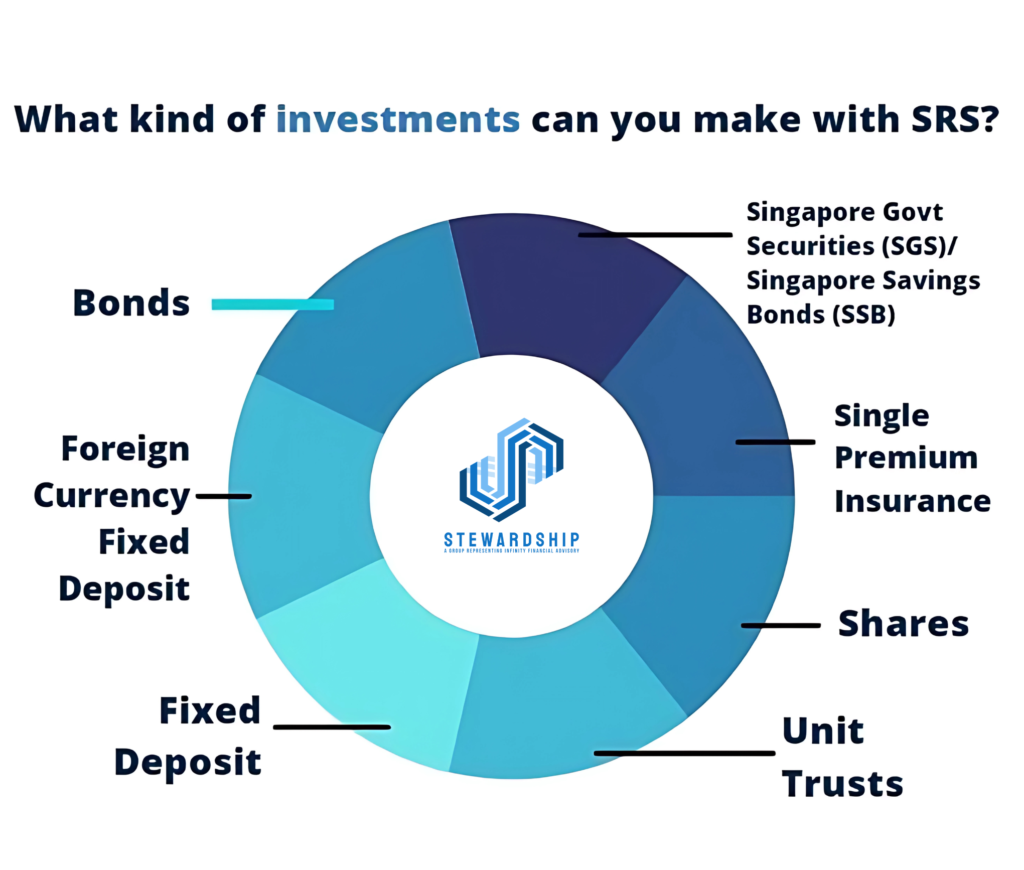

Using the SRS also gives you the added advantage of flexibility in choosing from a wide range of investment instruments which you prefer. Be it unit trust, stocks, fixed deposits or a single-premium endowment, depending on which you feel will give you the best returns and suit your needs, you are empowered to make your own choice!

However, a penalty applies if an early withdrawal is made, meaning that if you make withdrawals before the statutory retirement age, the amount withdrawn is subjected to taxes coupled with a 5% penalty. This is to discourage individuals from making withdrawals before retirement.

Contact us to understand more about the SRS and how it can fit into your financial plan. We can help you do a simple cost-benefit analysis to discover how much you can actually save and earn with this scheme.

*The prevailing retirement age in the year the first SRS deposit is made.

“ This advertisement has not been reviewed by the Monetary Authority of Singapore.

The information in this post is accurate as of its posting date.

The views expressed in this material may not necessarily reflect the views of Infinity Financial Services Pte Ltd. The information provided herein is intended for general circulation and are not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use will be contrary to local law or regulation. This material may not be copied, either in whole or in part, or distributed to any other person without our specific prior consent. Infinity Financial Services Pte Ltd and its affiliates, directors, associates, connected parties, employees and/or Representatives may own or have an interest in the securities that may be covered in this material.

Please seek advice from a Financial Advisor Representative or consult your professional regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to purchase the investment product. In the event that you choose not to seek advice from a Financial Adviser Representative or a professional, you should consider whether the product in question is suitable for you.”